|

Communications and Manuals of the GST Portal (www.gst.gov.in) is presented

here.

Click on the relevant link to view.

GSTR 1, 2, 3 Due Date for July, 2017

Extended

The Government has

notified the extended due dates for

filing of returns, GSTR 1, 2, 3 for

July, 2017 as follows :

|

Sl. No. |

Details/return |

Class of taxable/registered

persons |

Time period for furnishing

of details/return |

|

(1) |

(2) |

(3) |

(4) |

|

1. |

GSTR-1 |

Having turnover of more than

one hundred crore rupees |

Upto 3rd October, 2017 |

|

Having turnover of upto one

hundred crore rupees |

Upto 10th October, 2017 |

|

2. |

GSTR-2 |

All |

Upto 31st October, 2017 |

|

3. |

GSTR-3 |

All |

Upto 10th November, 2017 |

Click to view / download Notification

30/2017.

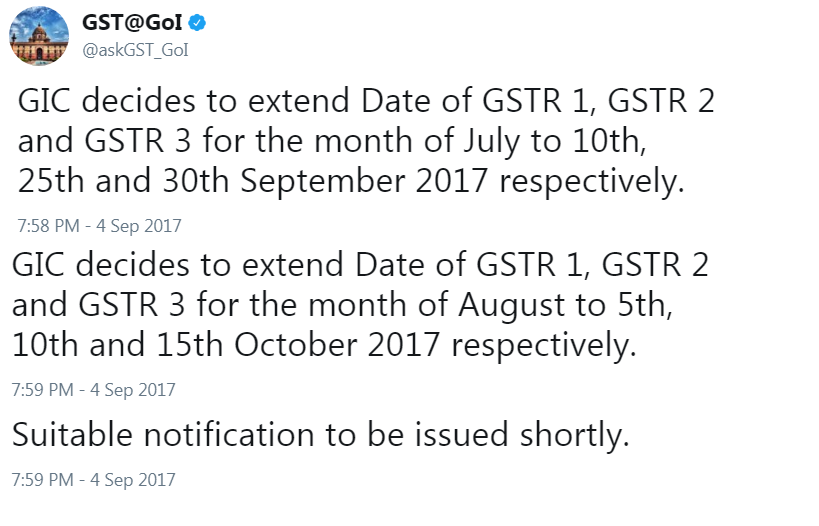

GSTR 1, 2

and 3 Due Date for July, 2017 and August, 2017 Extended

Here are the tweets on extension of due date for filing

of return in For GSTR-1, 2 and 3 for July, 2017 and

August, 2017.

Date:

04-09-2017

|

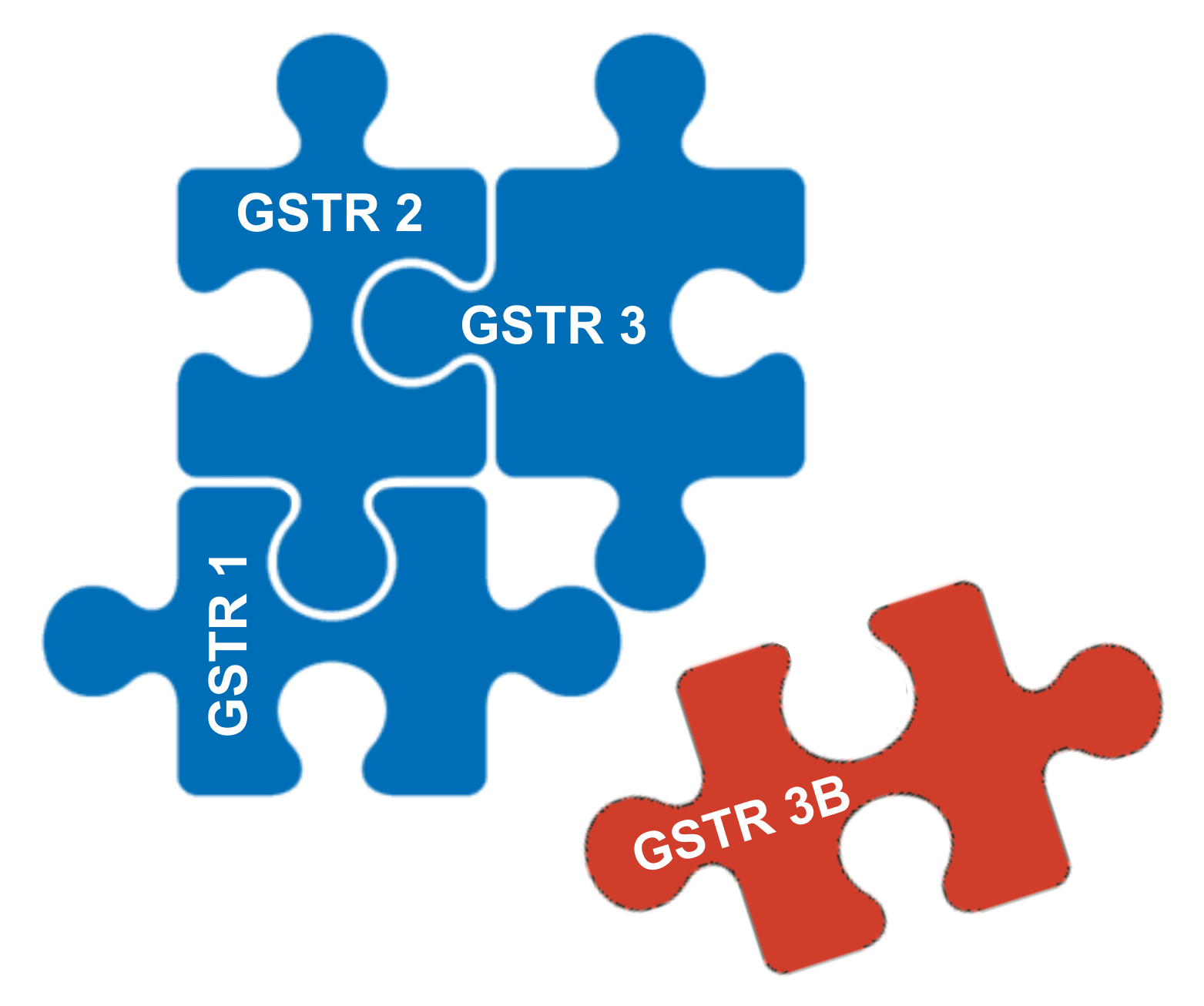

System based reconciliation of information furnished in FORM GSTR-1 and

FORM GSTR-2 with FORM GSTR-3B

The Central Board of Excise & Customs has issued Circular No: 07 of 2017 dated 01/09/2017 detailing the process of System based reconciliation of information furnished in FORM GSTR-1 and FORM GSTR-2 with FORM GSTR-3B for the month of July, 2017.

The circular explains in detail the process of Furnishing of information in FORM GSTR- 1, auto populating of details of inward supplies in Form GSTR-2A and adding information pertaining to details that are required to be furnished in GSTR-2 but are not part of FORM GSTR-2A like details of imports, details of supplies attracting reverse charge that have been received by registered person.

|

|

|

Here is the highlights of the Circular

Where the registered person has not submitted the return in FORM GSTR-3B, he is required to furnish the details in FORM GSTR-1 and FORM GSTR-2 and sign and submit the return in FORM GSTR-3 along with the payment of the due taxes together with interest on delayed payment of tax starting from 26th day of August, 2017 till the date of debit in the electronic cash and / or credit ledger. No late fee, however, would be levied for late filing of return Where the registered person has not submitted the return in FORM GSTR-3B, he is required to furnish the details in FORM GSTR-1 and FORM GSTR-2 and sign and submit the return in FORM GSTR-3 along with the payment of the due taxes together with interest on delayed payment of tax starting from 26th day of August, 2017 till the date of debit in the electronic cash and / or credit ledger. No late fee, however, would be levied for late filing of return

Where GSTR -3B has been submitted without payment of tax the return shall still be subjected to the reconciliation process as detailed in the circular. Such registered person should furnish the details in FORM GSTR-1, FORM GSTR-2 and sign and submit the return in FORM GSTR-3 along with the payment of the due taxes together with applicable interest. No late fee, however, would be levied for late filing of return.

Where GSTR-3B has been filed and applicable tax has also been paid by the due date the discrepancy between the data furnished in Form GSTR 3 B and return in Form GSTR 3 will be dealt with as follows:

(a) If there is any short payment of tax or excess availment of input tax credit, the same shall be paid with interest for the days delayed from 26/07/2017 to date of payment. Transitional credit availed by filing Form Tran -1 can also be used for adjustment of short payment

(b) If there is any excess payment if tax or short availment of input tax credit the same shall be carried over for utilisation in subsequent liability.

(c) The details furnished in Form GSTR 3 will be taken as the final figures.

Click to view /download Circular on

reconciliation of GSTR-3B

with GSTR-1, 2 and 3

Date:

02-09-2017

Click to view our

Guidance Note on Filling in Form GSTR

3B.

|